A lot of people have told me they're waiting for rates to come back down before they make a move. That's a reasonable instinct, but the honest, verified numbers say that plan deserves a second look. Here's exactly what I'm seeing, sources and all, no hype either direction.

The 60-second version

- Mortgage rates already climbed roughly three-quarters of a point off February's low (near a 1-year high) without a single Fed rate hike.

- Futures markets now price meaningful odds of a Fed rate hike at the July 29, 2026 meeting, up sharply from a month earlier. A rate cut this year is priced at roughly zero.

- Every additional half-point on a 30-year fixed loan costs roughly $33/month per $100,000 borrowed, an illustrative example, not an offer or a rate/APR quote.

Where rates were and where they are

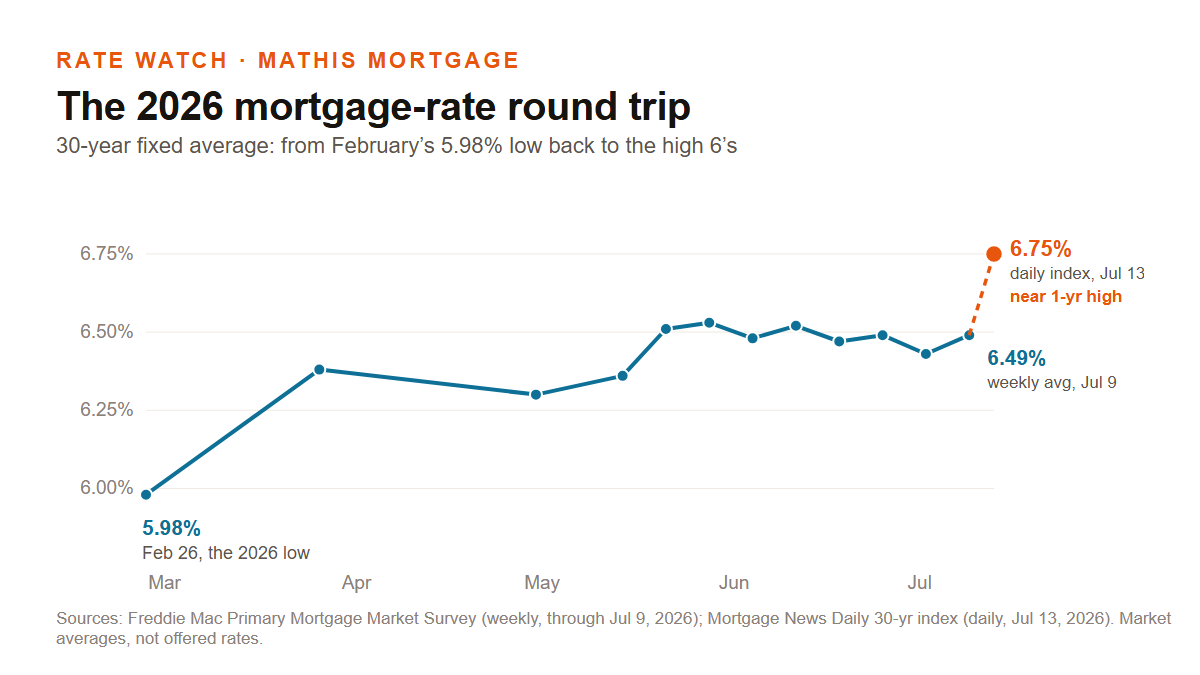

Back in late February 2026, the 30-year fixed average dipped to 5.98% (Freddie Mac Primary Mortgage Market Survey, week ending Feb 26), the first sub-6% reading in three and a half years. If you blinked, you missed it. Since then it's been a steady grind back up: the weekly Freddie Mac average sat at 6.49% as of Jul 9, 2026, and the faster-moving daily index from Mortgage News Daily hit 6.75% on Jul 13, 2026, which MND itself called "near 1-year highs."

The Fed just changed its posture

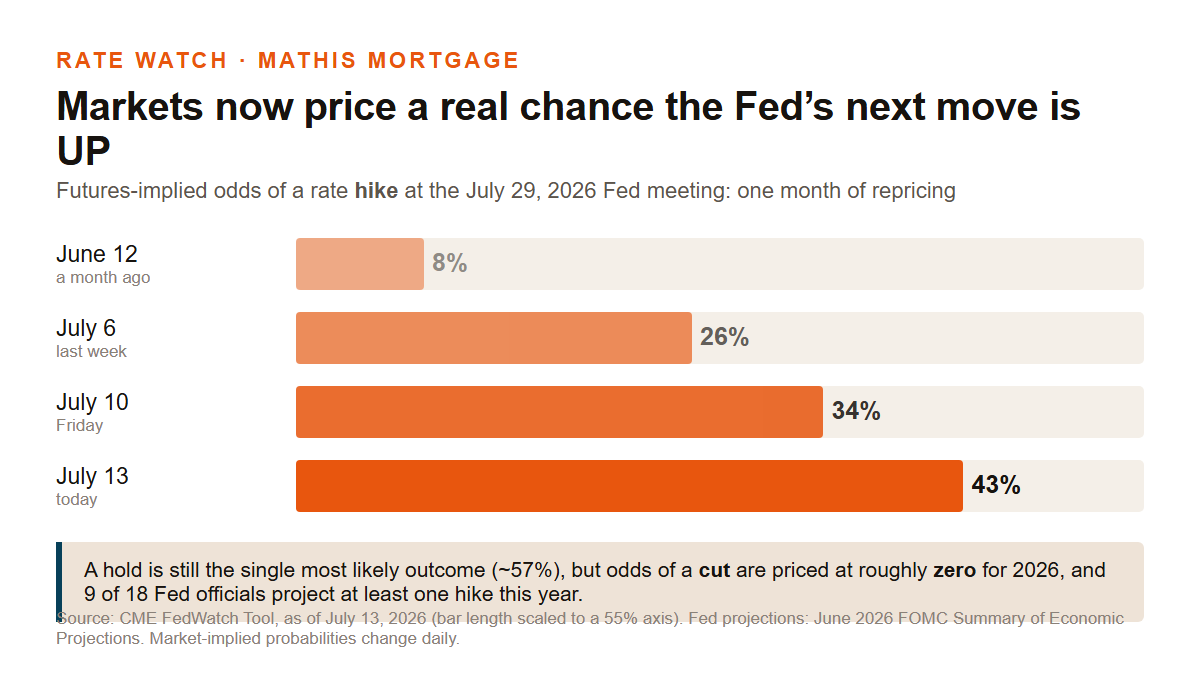

For two years the question was "when's the next cut?" That question is gone. At its June 17, 2026 meeting, the Federal Reserve held its target range steady at 3.50%–3.75% (a unanimous 12-0 vote, Chair Kevin Warsh's first meeting) but dropped its easing-bias language. The Fed's own June projections (the Summary of Economic Projections) now show 9 of 18 officials penciling in at least one rate hike before year-end, driven by an inflation outlook that moved higher, with projected 2026 core PCE inflation revised up from 2.7% to 3.3%.

The futures market noticed. CME FedWatch odds of a July 29 hike rose from about 8% on June 12 to roughly 43% as of Jul 13, 2026 (Polymarket showed a similar shift, pricing hold as still-favored but a hike as a live, rising scenario). Cut odds for 2026, across both markets, sit near zero.

Straight talk: a hold is still the single most likely outcome on July 29. Nobody knows for certain what the Fed will do, including the Fed. But here's the part that matters if you're waiting: the market has essentially stopped pricing rate cuts for 2026. The "just wait for cuts" plan doesn't have the data behind it right now.

Why your rate doesn't wait for the Fed anyway

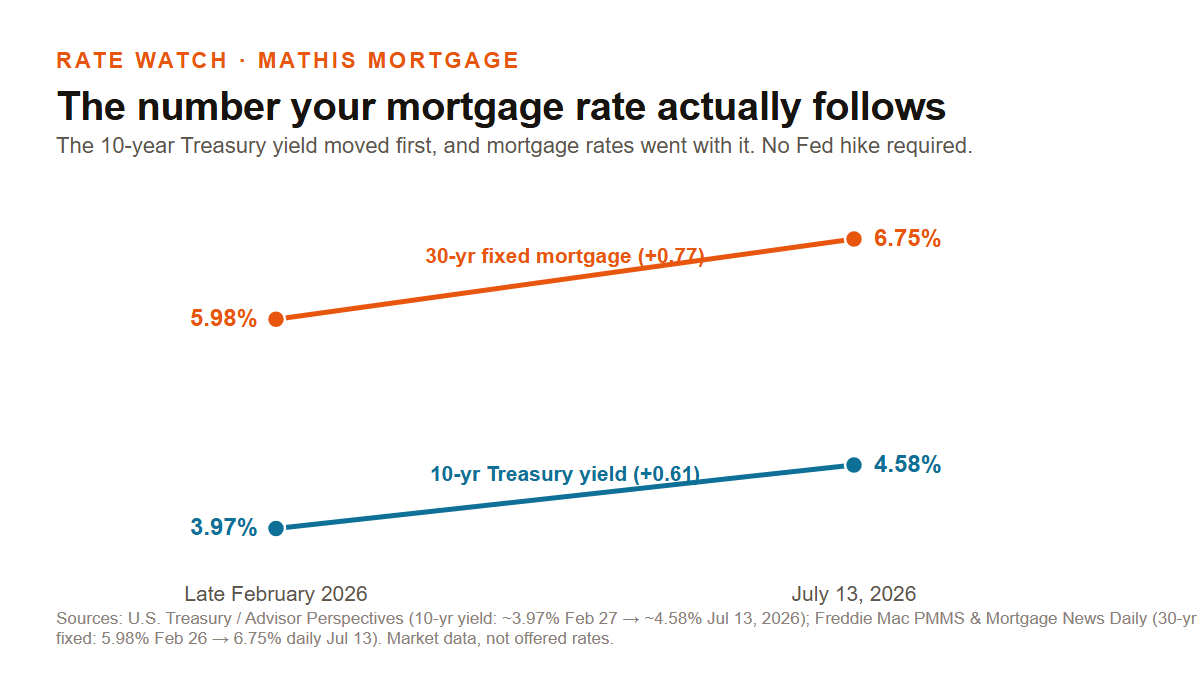

Here's the part most people don't know: your mortgage rate doesn't follow the Fed's target rate directly. It follows the 10-year Treasury yield, which moves on inflation expectations every single day, independent of what the Fed does at any given meeting. That's exactly how mortgage rates rose three-quarters of a point this year while the Fed did nothing at all: the 10-year Treasury yield went from about 3.97% in late February 2026 to about 4.58% as of Jul 13, 2026, a move of roughly 60 basis points that mortgage rates tracked closely.

Translation: if inflation keeps surprising to the upside, mortgage rates can keep drifting up whether or not the Fed ever raises its own rate. Waiting for a Fed decision is watching the wrong scoreboard.

What the professional forecasters say

Forecasts are educated guesses, not guarantees. But it's worth noting what's missing from them. As of their June 2026 forecast, Fannie Mae projects the 30-year fixed averaging around 6.4% for the rest of 2026, with a similar 6.3%–6.4% range persisting through 2027. The Mortgage Bankers Association's forecast is similar: roughly 6.5% on average through 2026, 2027, and into 2028. Neither organization is forecasting a return to sub-6% rates. The industry's own read, in plain terms, is that most of the rate relief is already behind us.

The math: what another half-point costs

If rates rise another 0.50% while you wait, here's the extra cost on a 30-year fixed loan (principal and interest only). These figures are an illustrative example, not an offer or a rate/APR quote: your actual rate, APR, and payment depend on your qualification and program terms.

| Loan amount | Extra / month | Extra / 30 years | Buying power lost |

|---|---|---|---|

| $400,000 | +$133 | +$47,858 | –5.0% (~$20K) |

| $500,000 | +$166 | +$59,822 | –5.0% (~$25K) |

| $600,000 | +$199 | +$71,786 | –5.0% (~$30K) |

| $750,000 | +$249 | +$89,733 | –5.0% (~$37.5K) |

Rule of thumb: every half-point of rate movement costs about $33/month per $100,000 borrowed, and shaves roughly 5% off what the same monthly budget can buy. That's only half the cost of waiting, too: if home prices rise even 3% while you sit out, a $500,000 home costs about $15,000 more to buy on top of financing it at a higher rate.

So what would I actually do?

Not panic, and not gamble. Three moves, all reversible:

- Get rate-ready now. A full pre-approval means that when your number shows up, you can lock it that day instead of scrambling for two weeks while it disappears.

- Know your number. Not the headline average: the payment that actually works for your budget. Figure out the rate that produces it, and let that become your green light.

- Put someone on watch. Rates move daily; if you have a target number in mind, it helps to have someone tracking it and flagging when the market touches it, in either direction. If rates fall later, refinancing may be an option, subject to qualification. If they rise, you'll be glad you didn't wait.

Talk to Randy

If you want the honest read on where your number sits today, let's talk it through. Call or text me at (949) 990-6030 for a no-obligation rate-readiness check: no credit pull, no pressure, just the numbers that apply to your situation.

Disclosures: Randy Mathis, NMLS #1516760 | DRE #02236644. Lumin Lending, Inc., NMLS #2716106 | DRE #02291443. Equal Housing Opportunity. Licensed in AL, AZ, CA, CO, ID, MD, MI, OR, PA, TN, TX, UT, WA. This is not a commitment to lend or a rate/APR quote. Payment figures above are illustrative examples of the difference a 0.50% rate change makes on a 30-year fixed loan (principal and interest only) and do not represent an offer of credit; your rate, APR, and payment will depend on your situation. All loans subject to credit approval, income and property qualification, and program terms. Data as of July 13, 2026. Mortgage rates and market conditions change and should be independently verified before relying on them.